December 2012 Market Update

While the national housing market is improving, there are still signs that indicate we are not yet experiencing a full-force recovery. Credit standards are still tight. There are millions of homeowners in some stage of foreclosure or default, while millions of others still owe more than their homes are worth. As long as the economy continues to strengthen, the housing market will move toward the recovery we have been waiting for. However until the recovery is fully realized, we must remain aware that if the economy weakens again, the housing market could relapse.

The Federal Housing Administration announced that as a result of so many mortgage delinquencies, it might have to exhaust its reserves, which could result in the FHA needing to rely on taxpayer funds for the first time in its 78-year history. A government bailout of this magnitude could possibly weaken the economy, but the U.S. Treasury will not make a decision until next February.

Considering the current, stringent mortgage underwriting standards, it’s important to know how credit scores work; improving your credit score will increase your likelihood of obtaining financing. NAR President Gary Thomas states, “Record-low mortgage interest rates shouldn’t be taken for granted.” Buying a home now is favorable for those that want to take advantage of interest rates while they are at historic lows.

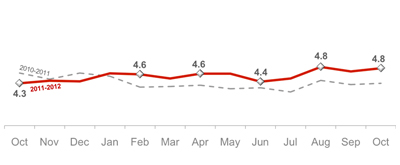

Home Sales

In Millions

Home sales were up 2.1% this month to a seasonally adjusted rate of 4.79 million units, a 10.9% increase from last year. NAR Chief Economist Lawrence Yun mentions that Hurricane Sandy had some impact on sales figures this month. He states, “Home sales continue to trend up and most October transactions were completed by the time the storm hit, but the growing demand with limited inventory is pressuring home prices in much of the country. We expect an impact on Northeastern home sales in the coming months from a pause and delay in storm-impacted regions." Distressed homes (which include short sales and foreclosures that traditionally sell for 15%–20% less on average compared to nondistressed homes) accounted for 24% of October sales, unchanged from the previous month; they were 28% in September 2011. The amount of distressed properties are high by historic standards, regardless of their seemingly stable percentages.

.

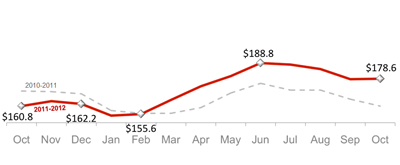

Home Price

In Thousands

The median home price fell again in October to $178,600, compared to the previous month’s median price of $183,900. Home prices are up 11.1% from a year ago, which marks the eighth consecutive month of year-over-year price gains, which hasn’t been seen since October 2005.

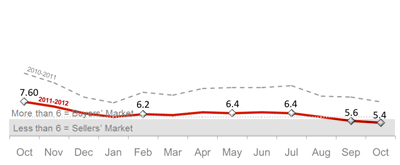

Inventory- Month's Supply

In Months

Housing inventory fell 1.4% from Septembers to 2.1 million existing homes available for sale, representing a 5.4-month supply. Inventory levels are down 21.9% from last year’s 7.6-month supply, which is the lowest supply since February 2006.

Source: National Association of Realtors

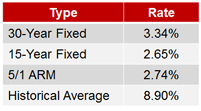

Interest Rates

Interest rates this month continue to decline at or around 3.34%, reaching record lows. NAR President Gary Thomas states, “Even with rising home prices, we’ll continue to see favorable housing affordability conditions over the coming year, but they won’t last forever. Inflationary pressures are expected to build during the next two years. As a result, mortgage interest rates will also rise with inflation. Buyers who are currently held back by tight mortgage credit standards should work to improve their credit scores, so they'll be able to qualify for a mortgage while conditions are still favorable.”

This Month's Video

Contact me,

your local real estate expert,

for information about what's going on in our area.